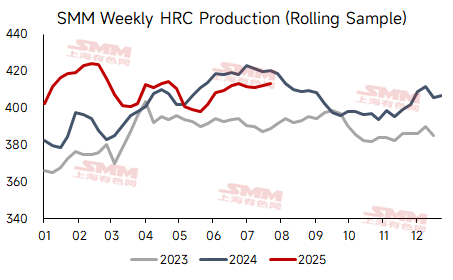

• HRC production in July rose 1% MoM, and was lower YoY.

According to SMM data, the weekly average domestic HRC production in July was 4.1199 million mt, which was lower compared to the same period last year, and rose slightly by 0.8% MoM from June.

- Steel mill profits expanded in July, with the average monthly profit growth of hot-rolled coil and rebar reaching nearly 40%.

From the profitability perspective, steel mill profits expanded MoM in July. Specifically, hot-rolled coil profits increased from an average of 201.96 yuan/mt in June to 292.83 yuan/mt, while rebar profits increased from an average of 155.75 yuan/mt in June to 204.53 yuan/mt. The MoM increase in profits boosted steel mills' production enthusiasm, leading some steel mills to postpone maintenance.

- Maintenance impact at steel mills declined significantly in July and may increase slightly in August.

According to SMM's statistics on steel mill maintenance, the impact from HRC maintenance in July was approximately 259,800 mt, a decrease of 257,200 mt MoM from the previous month. The announced impact from HRC maintenance in August currently stands at 265,600 mt, an increase of 5,800 mt MoM. Maintenance is concentrated in the north-east and northern China regions. In August, steel mills in the Beijing-Tianjin-Hebei region may be subject to production restrictions due to policies such as the military parade, but other regions have limited policy impacts. Driven by high profits, production enthusiasm is generally high. Additionally, with the recent increase in ferrous metals series prices, downstream purchase willingness has improved, and most steel mills have good domestic trade order-taking situations. Overall, it is expected that domestic HRC production will continue to fluctuate at a medium-high level in August.

Overall, the supply elasticity of HRC in August is relatively small, continuing to fluctuate at a medium-high level. Demand is entering the end of the off-season, with limited room for further reduction. There is no immediate risk in short-term exports, and it is expected that the accumulation of HRC inventory in August will be limited. On the macro side, two major events have recently occurred both domestically and internationally: the extension of China-US tariffs for another 90 days and the conclusion of the domestic Political Bureau meeting. Market expectations for important meetings in the second half of the year have risen. In the short term, the fundamental contradictions in the steel market are relatively small. With a positive macro sentiment and support for raw material price trends under high hot metal production and high profits, the overall steel price floor is relatively solid. It is expected that the current round of price corrections will be limited. Attention should be paid to subsequent events such as "anti-rat race competition" and "military parade" trading, as well as hot metal production trends and export changes.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)